Listen and subscribe

Apple  Android

Android

In this week’s episode, Dave, Cate and Pete take you through:

What will the property market do in 2021?

- Pete – PREDICTION – Every capital city will see increases for 2021 higher than 2020

- Dave – PREDICTION – Broadly speaking we expect all the capital cities to perform quite strongly.

- All – PREDICTION – The market will rise – why?

- Pete – availability of finance, lending rules were going to be eased (adjustments to responsible lending), allow people easier borrowing, interest rates are low, consumer confidence is on the rise.

- Dave – debt serviceability is at a 19 year low, this is part of the puzzle feeding into the market. Interest repayments as a share of household income is the lowest it’s been since March 2002. Billions of stimulus money – home builder, government incentives, stamp duty concessions, new build stimulus.

- Cate – covid has had an impact, people have saved a lot of money and have heightened borrowing capacity because of buffers being relaxed, dropped from 7.5% to close to 5%.

These did eventuate

What will the property market do in 2022?

- Pete – PREDICTION – 2022 will see positive capital growth for capital cities and regional areas, but not as good as 2021.

- Cate – PREDICTION – I think regional and capital cities will outperform for 2022, not prepared to say it will be less than 2021, I think it will be a heady year. Disclaimer: provided that we don’t see any shocks to the market. There is quite a lot of buyer hunger, record low interest rates. I don’t think that tiny regional cities will go hard, especially those that don’t offer easy commutes and jobs.

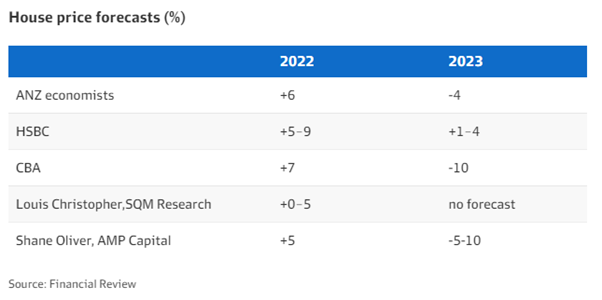

- Dave – PREDICTION – Oz wide rise by 7 – 12%. I think most, if not all capital cities will underperform 2021 increases. Slightly above what most of economists are predicting – 3 to 10%. I think it could surprise and be double digit growth again.

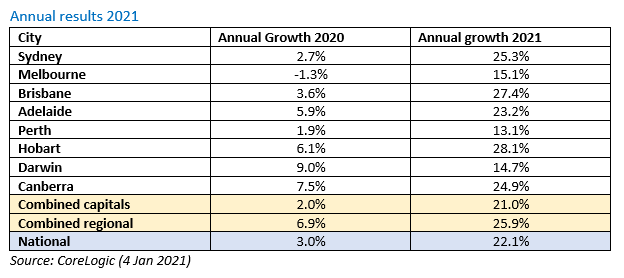

Capital city top performers in 2021

- Dave – PREDICTION – Melbourne to finish in the top 3, many economists tipping it to come last but don’t think this will be the case because it dropped further and it had an extra lockdown, so it has more room to move on the upside.

- Dave – PREDICTION – Perth, with price of iron ore could be number #1. It’s been so flat for so long and driven by mining (which is not a good thing as you want to look for long-term performance), but for the next 12 months it’s a strong chance.

- Pete – PREDICTION – Perth, will be number #1 or close to number #1, it’s been a long time down in the doldrums, iron ore, number of listings is down so supply is down and rents have gone up significantly in Perth. Not dependent on migration or tourism, unlike other capitals.

- Pete – PREDICTION – Adelaide will be a strong performer, but not as strong as Perth.

- Cate – PREDICTION – I think Melbourne will bounce back and be in on the top #3 and potentially be number #1. Risks of migration and study will be an issue, but there will be a big bounce back. Despite businesses suffering, there are a lot of highly paid people in Melbourne with increased savings.

- When we made these predictions, we thought Melbourne had come out of the storm, zero cases and lockdowns were over. However we had a similar year of lockdowns in 2021, that we saw in 2020, which we didn’t think would happen. In terms of Perth, the boarders were closed for the whole year and this held Perth back as well.

- Cate – PREDICTION – Hobart is a compelling place for working remotely and the lifestyle offered there. Hobart probably has a bit in store and we should keep an eye on Brisbane and regions, a lot of people have decided to do the northern migration.

- Well done Cate! This was spot on.

Capital city top performers in 2022

- Cate – PREDICTION – Melbourne is going to spring back – I really do think it will play catch up when the international borders reopen and students come back. My rationale relates to the sheer buyer demand. Even in the face of high listing volumes and lots of social distractions in December 2021, Melbourne still only came off 0.1%, which I think is miraculous. Melbourne will be in the top 3 or the top 2.

- Also –

- Hobart – love affair is still there, no stock and vacancy rates

- Brisbane – every reason to keep performing

- Canberra – what-ever happens in May with the election could get things along or dampen

- Pete – PREDICTION – TOP FOUR – Adelaide, Brisbane, Hobart, Regional Areas.

- Dave – PREDICTION – Brisbane momentum will continue to hold on to top spot for 2022, Adelaide has solid momentum, Perth. (subject to Perth borders opening from Feb as has been decided and staying open all year) and highly sought-after coastal areas around the country. But I think once all beachside locations peak, we will see a long flat period of minimal and or negative growth for many years. Hobart continues to have stock shortage, I’ll share that with listeners and socials soon, I did think Melbourne was going to recover and it’s a buying opportunity, but it may play out over more than 1 year. Melbourne’s median value has dropped below Canberra, significantly lower than Sydney historically, I think the stigma of shut downs and also the desire to escape the potential for future covid lockdowns, that not as many will come to Melbourne from interstate in the next 12 months, but it will rebound over time. I’m also worried about stigma from Perth and having borders shut all the time.

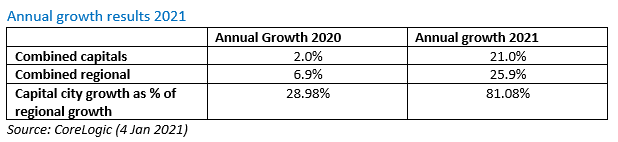

Regional locations – 2021

- Cate – PREDICTION – Continued level of performance out of our regions – maybe not at the same rate.

- Was wrong there as regions outperformed.

- Cate – PREDICTION – We will see a stark contrast between houses and townhouses vs apartments.

- Units were in the 20% as well, people were buying what ever could get their hands on.

- Cate – PREDICTION – Top quartile property price growth will slow down in regions, as the appeal of capital cities shines bright again, the bottom quartile will start to perform and speed up because of a return of investors. People love bottom quartile properties in regional market when looking for strong cash flow. Strong rental returns and capital growth in regions will entice investors.

- Half wrong and half right there, the bottom quartile has gone hard, but the top quartile has also continued to shine bright. There was a continued flee away from the city. The two regions that I’m familiar with, their top quartile properties have gone strong.

- Dave – PREDICTION – Capital cities will start to close the gap on regionals, people will come back to capital cities once normality resumes and to make up on time lost during lockdowns – likely to be in line with when vaccines are available. Capital cities may start to outperform the regions again.

- Capital cities did close the gap but didn’t surpass them. We did have more lockdowns that we were not expecting, which was a bit naïve of us. Vaccine roll out was a story of the year, but we didn’t get there until the end of the year. Some capitals outperformed regionals, but majority did not.

Regional locations – 2022

- Pete – PREDICTION – Regional areas will outperfrom capital cities again, 3 years in a row – covid-19 and wfh exodus. Not any country town, they have to be within reasonable distance of capital city, lifestyle attributes.

- Cate – PREDICTION –

- Ratio between houses and units, not a severe ratio in regions but was in metro – for metro the gap will close, units will come back.

- Regional growth will continue in the significant regional cities, not tiny ones, populations less than 20,000 for a regional town particularly more than 90 mins away from capital city or hub I am really nervous about

- Rate of holiday house take up will slow down as international borders open up.

- Dave – PREDICTION – Fairly even, the gap could continue to close but not saying that with any confidence. Double whammy of demand with exodus and also the well off in capital cities desire for buying holiday getaways is still there.

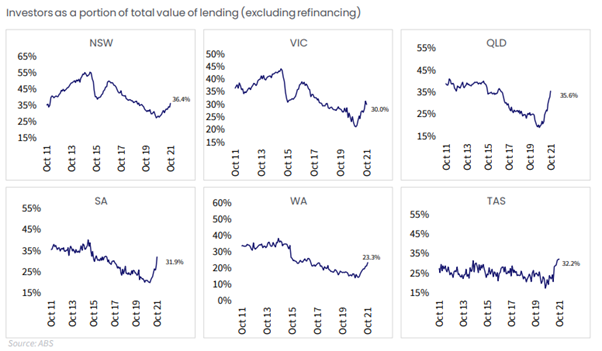

Investor numbers – 2021

- Dave – PREDICTION – We’ll see investors bully their way back in and investors numbers to increase in 2021. The appeal of neutral and positive gearing will spur investor activity.

- Cate – PREDICTION – with the cost of doing business being reduced, investors will come back into the market. Returns and low interest rates – this will be the year of returning investors.

- Pete – PREDICTION – with HomeBuilder being phased out by March, we’ll see the end of first home buyers, especially for new homes, which leaves the gate open for investors.

- All correct on that point – that’s what the three of us have in common, we know what investors are up to, that is our thing.

Investor numbers – 2022

- Pete – PREDICTION – Assuming APRA doesn’t place restrictions on investment, investor numbers will continue to increase but not at the same rate as 2021.

- Cate – PREDICTION – investor numbers to increase unless the regulator toys with credit policy and restricts it again, but I think they know that it’s a dangerous thing to do in the face of really tight vacancy rates.

- Cate – PREDICTION – I think we’ll see some policy to target investors to entice them to be a part of an initiative to offer affordable housing.

- Dave – PREDICTION – Yes, continue to increase and this to become a political issue, lots of articles written about it, some kind of policy intervention during the year to slow down – whether it’s APRA broadly making it harder to borrow or something specifically to target investors.

APRA intervention in the property market – 2021

- Cate – PREDICTION – at some stage in late 2021 or early 2022, we’ll start to hear people campaigning for easier conditions for first time buyers.

- We haven’t had strong campaigns for first home buyers – continued with some incentives for them and they are still active.

- Dave – PREDICTION – I think Middle of 2021, noise in the media about price property affordability, the jungle drums will keep beating and APRA will step in late 2021 or early 2022.

The results: 6 Oct 2021 – APRA increased minimum interest rate buffer (assessment rate) from 2.5% to 3% and for ADI to implement this by end of October 2021, or prudential capital requirements would be adjusted for each ADI that did not.

APRA intervention in the property market – 2022

- Pete – PREDICTION – No.

- Cate – PREDICTION – Not in 2022. If we have a record runaway market, I predict they’ll do something more aggressive in 2023.

- Dave – PREDICTION – Yes, especially if rates stay at the same level all year – either APRA restrict lending to some degree OR new government policy designed to increase supply, assist first time buyers OR restrict investor numbers. The media is too powerful nowadays and there will be promises made. The policies that come out will be dependent on which party wins the election.

Developers and building – 2021

- Pete – PREDICTION – Developers and builders will be flat out, if you get the homebuilder grant, the build has to start in a certain period of time. If you’re looking for a tradie or builder, you’ll be hard pressed to find one and be prepared to pay more. This will be fantastic for the economy.

- Dave – PREDICTION – shift to larger size apartments and townhouses and less one bedroom apartments, more two bedroom apartments.

- The last census showed that the property type growing at the largest scale was townhouses.

- Cate – PREDICTION – Penthouses and 3 bedroom apartments to recover and exhibit growth, because they’re rare. People want the extra bedroom. Bedsits and 1 bedroom apartments will languish.

- Cate – PREDICTION – developers will up the ante for business to get apartments sold, they will be offering more than just TV’s and VISA cards.

- Cate – PREDICTION – there will be a builder shortage due to many choosing to extend homes.

Developers and building – 2022

- Pete – PREDICTION – 2022 will continue to be a tough time to find a tradie or builder. Some builders will go under due to cashflow issues, brought on for supply (eg: if supply is hard to get, you can’t proceed with building, if you can’t do that, you won’t get progress payments)

- Cate – PREDICTION – I think builders and materials will remain in tight supply. Renovation/build costs will continue to influence up-sizers to sell/buy as opposed to renovate. I also worry about developers and builders with fixed price contracts – I’m fearful we’ll see a few go under and this will exacerbate the builder shortage issue. We also have so many exciting infrastructure projects and investment going on in the country – I personally know that many in the building trade are opting out and swapping to contract work for the project managers of the successful incumbent infrastructure companies – continued issue which will be a hallmark of 2022 and it will see a lot of people choosing to sell and buy, as opposed to renovate and extend.

- Dave – PREDICTION- Builders continue to be very expensive due to the overhang of the home builder, continuing and supply chains not untangling as easily as many thought or hoped.

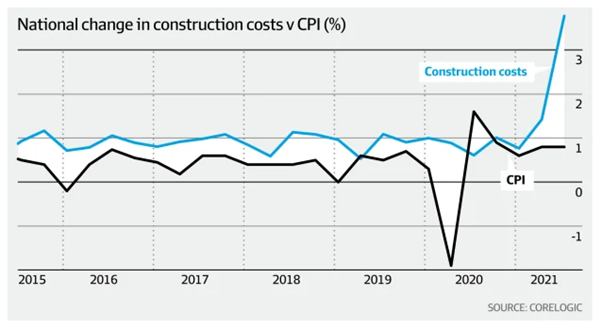

Interest rates – 2021

- Dave – PREDICTION- Interest rates – continue to stay low. One of the potentials for the stimulus is that low rates can create asset bubbles, could be looking at an inflation issue (maybe 2 years, could be 5 years). In short to mid-term interest rates will remain low. Dave mentioned the fact that one in 5 USD in circulation were printed through the stimulus of 2020.

- Fixed rates are lower than they have ever been, this is the best time to lock in fixed rates. Often lower than what you can get for variable rates.

Interest rates – 2022

- Pete – PREDICTION – The cash rate will remain the same

- Cate – PREDICTION – No change in 2022 for cash rate unless US inflation becomes a consistent concern. If there is an increase it will be tiny, 0.25% is really big considering the cash rate is now 0.10%. Fixed rates to increase.

- Dave – PREDICTION – Remain at the same level, or a rate rise of 0.25% in the second half of the year. RBA to announce the end of QE measure after the first RBA meeting – in Feb 2022.

- Dave – PREDICTION – fixed rates continue to increase further

- Dave – PREDICTION – US will increase 3 or more times and that will put pressure on rate increases on countries like Australia and the Aussie $

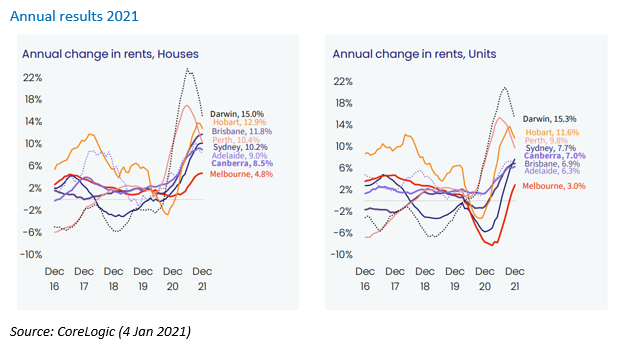

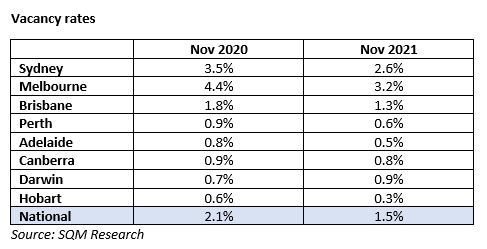

Rents and vacancy rates – 2021

- Cate – PREDICTION – Tenants to return, vacancy rates to tighten

- Seeing record low vacancy rates

Rents and vacancy rates – 2022

- Pete – PREDICTION – Rents to continue to increase and vacancy rates to stay extremely low, international students come in and borders open.

- Cate – PREDICTION – Higher rents and tighter vacancies EVERYWHERE and I feel Melbourne’s bounce back will shock us all.

- Dave – PREDICTION – Rents increasing at a more stable pace, but above average. Increasing investor purchases will put downward pressure on this gradually over the year and policy intervention, but the return of international migration and overseas students to more historical numbers will offset this.

- Vacancy rates remaining very low which will also be partly due to the lag time of new properties being finished due to slowdown in 2020 of new projects.

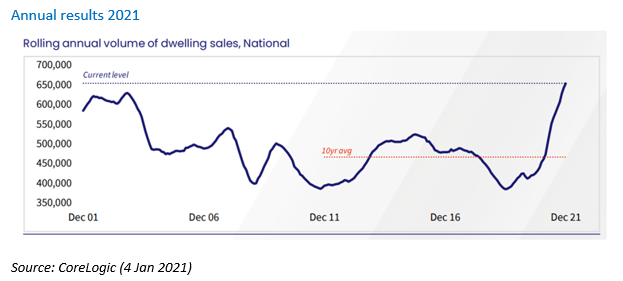

Sales volumes – 2021

- Pete – PREDICTION – Increase in the number of sales

- Cate – PREDICTION – Increase in listing numbers in metro when vendors see that selling conditions are good.

Sales volumes – 2022

- Pete – PREDICTION – Remain high but it won’t be a record year like 2021

- Cate – PREDICTION – Higher than previous 12 months, but I predict lower sales volumes. I think we’ll see greedy vendors trying it on, but not all will meet the market. Some of the smaller properties, anything that an upgrader is selling, we’ll see a fair few of those.

- Dave – PREDICTION – Reduce, but stay above the average sales volumes from the last 3 to 5 years. 2021 was the highest on record, don’t think that’s going to happen again this year.

Risks impacting the market – 2021

- Cate – opportunity to buy at a reduced rate when JobKeeper comes off, this pales in comparison to the driving forces. There could be some fall out from that. I’m of the view that vendors who have been in distress, will have made a sensible decision and taken measures to clear their debt or downgrade their property.

- Dave – there may be another level of support for small businesses. Geopolitical risks are China relations and Iron Ore and what that will do for our exports.

- Pete – risk that vaccinations are not the panacea that people are expecting. Vaccines have started to roll out in some nations and the results are looking positive. Providing this continues to do ok, the economy will continue to perform well and so will property prices.

Risks impacting the market – 2022

- Pete – PREDICTION – Tightening of lending

- Cate – PREDICTION –

- Any silly stuff our politicians dream up to win votes,

- APRA tinkering with credit

- US hiking up interest rates

- Builders with fixed price contracts going into receivership

- Another nastier COVID strain than Delta

- Supply chain shocks with essentials and panic buying

- Dave – PREDICTION –

- Inflation becoming endemic EG continuing for the first 6 months of the year, and maybe longer.

- New Covid strains and Covid still not becoming something we can live with easily and freely.

- Supply Chains not freeing up as easily as some believe they will. US increasing rates multiple times.

- Share market falling in the US and OZ.

- Oz increasing rates early.

- Russia invading Ukraine.

- APRA stepping in again or government placing restrictions on investors.

- Perth and Melbourne are on the nose due to the Government’s harsh approach to lockdown and closed borders causing trust issues for interstate migration.

- Property market moving into negative territory towards the end of the year.

- I predict some of the above will occur:

- * US rates rising multiple times in 2022. China asking US and others not to raise rates.

- * Supply chain issues lingering for at least 6 months, if not all year.

- * Inflation challenges lingering for at least 6 months, if not the entire year due to the supply chain issues and the amount of new money printed/QE as part of the unprecedented stimulus of 2020 and 2021 that may yet become a new historical lesson to learn for future economists and governments.

- * Further measures to curb lending by APRA or to specifically target investors/help FTB’s by APRA or government.