Plotting Australian property market movements from 1970 to now

- Property Planning Australia

- May 30, 2022

- 7 min read

Updated: Mar 31

The impacts of recessions, inflation, financial deregulation, population growth, unemployment rates and analysing what could disrupt the drivers of price increases? (Episode 155)

In this week’s episode, Dave, Cate and Pete take you through:

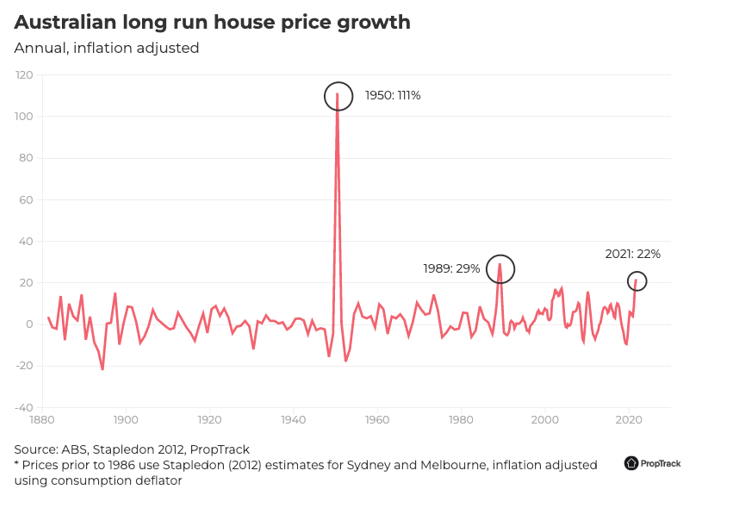

A look at Australia’s price spikes Since the 1950’s, Australia has seen 3 periods of stellar growth. The most mind-boggling being 1950, where prices grew 111%! What were the drivers of growth and how have these forces changed over time?

Disrupting the property market Fast-forward to today’s drivers of capital growth, it seems that proximity to the city will continue to be a key factor for desirability, competition and property price growth. With more households sustained by double incomes, convenience and being close to amenities has been more important than ever. The trio discuss what could shake up the status quo.

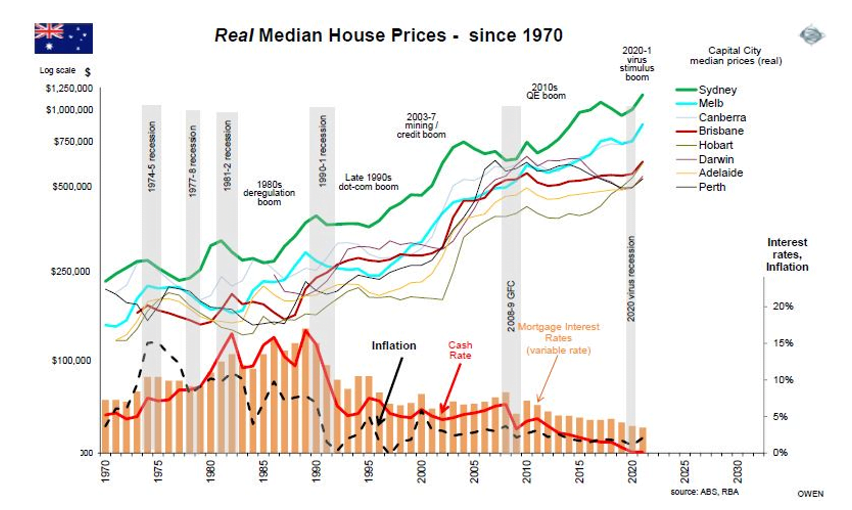

Diving into Australia’s recessions The trio discuss the recessions from 1970’s to now, what caused them, what were interest rates doing at this time and how these features compare with our nation’s situation today.

How financial deregulation has impacted the property market The trio look back to 1980’s which saw an upheaval in banking regulation and how this impacted the economy and property market. After all, Australia held the mantel for the country with the longest period of time without a recession.

How has population growth impacted capital city prices? Does population growth have a direct correlation to capital growth? The trio dive into the data to answer this question.

How have capital city prices on the ladder changed over time and which cities displayed more volatility than others? The trio discuss the movements of capital cities from 1970 and how each have performed. Interestingly, Perth has been near the top of the ladder a few times, highlighting the power of employment, natural resources and availability of high-paying jobs. Check out our show notes for a great infographic that shows the growth of capital cities in inflation adjusted dollars.

Why property is a great asset class to invest in The trio discuss the history of property prices in relation to inflation and why investing in property is a solid move and a great hedge against inflation.

Resources

Check out the infographic on Australian Capital City House Prices

Ep#25: Why is property a good asset class to invest in

Ep#46: Recovery lessons from recent recessions, the great depression, GFC & Spanish Flu

Ep#73: Dissecting 10 years of Core Logic data – capital cities & regional areas

Ep#111: Property Booms and Price Drops in Australia from 2003 to 2021

Ep#121: How supply and demand dictate market movements – Part #3 Locational drivers – Superstar cities, population paradox, NIMBYism, zoning, development, yields, vacancy rates, heritage overlays, regionals and more!

Four critical mortgage offset strategies

Five mortgage strategies that can grow your wealth

How will your mortgages serve you in the long run?

How our mortgage strategy helps us to hold properties

How to succeed with Property and Create your Ideal Lifestyle

Show notes

3 biggest price spikes in our history

1950 – 111% growth: people knew they could buy and sell for a better price, there was a lot of speculating, didn’t even have to do a renovation to make a profit.Before the 1950s, land on the fringes of urban cities was both close to CBDs and relatively cheap, which kept a lid on house prices.Once land close to cities became more scarce, along with the high levels of immigration into Australia in the 50s, 60s and 70s, prices started rising at a faster rate.” Then people started buying cars.

1960 – explosion of suburbia, freeways and highways were developed and cars became cheaper to buy.

1989 – 29% growth

2021 – 22% growth

In the 2000’s – not a huge move, but there is a move back to get closer to the city as well.

The work force has changed – two parents working there. When I was a kid, mum was at home and if dad got home late, he came home late. These days picking up kids from school and don’t want to sit in traffic for an hour.

There’s a real value around getting closer activities – and you pay for it.

Being close to the city will continue to be a driving factor for capital growth – high concentration of jobs and amenities, until there is a sustained reliance on working from home, creating other hubs or a form of transport that supersedes what we do now.

1974/75 recession: what caused this?

The major influence of the experience of the 1974 recession came in the form of the concept of stagflation, that is, inflation during a period of recession.

For the economy, 1974 was the end of the good times. It was the year the Commonwealth budget exploded. As the Whitlam government pressed on with its big-spending reforms despite Treasury pleas for restraint, Commonwealth spending surged 46 per cent in 1974-75, dwarfing the 20 per cent rise the year before.

Similariites with covid big spending

Recessions. 1974–1975: The mid-1970s recession followed a global oil price shock in which the world price of oil roughly quadrupled. The increase in world oil prices generated high rates of inflation which were made worse by domestic wage pressures. Triggered by wars in the middle east.

Although unemployment was in the 2% this time.

1981/82 recession: why so many recessions in one small time frame?

A key event leading to the recession was the 1979 energy crisis, mostly caused by the Iranian Revolution which caused a disruption to the global oil supply, which saw oil prices rising sharply in 1979 and early 1980.

The highs of the 80’s and 90’s crisis:

Interest rate hit 17.5% – Dad was worried that it would hit 20%

90’s recession is probably the worst one

Middle management who lost jobs and bought stores or franchises. Inflation above 10%, unemployment above 10% and interest rates in the high teens. That was a killer. In comparison, the GFC didn’t’ last long and Covid recession was only 6 months and plenty of government support.

Financial deregulation: 1989 – big impact on the property market and what’s happened since then. Banking and financial systems more flexible and ease of access to finance. Which has also done well for the economy – until recently we had the longest period of time without a recession

Joined the mortgage broking industry in 1999 – hardly anyone knew what a mortgage broker was then, now 2/3 of all loans done through mortgage brokers. Rise of offset accounts – that provides opportunity for protecting and creating wealth

Deregulation of the finance system

Floating of the Aussie dollar

Banking crisis

Impact on commercial property

Resultant recession

How has population growth impacted capital city prices?

Population does not affect property prices – property prices went bonkers during covid, even though we had no new entrants.

There is more than just one thing that affects the property market.

It highlights significantly, that population is not the only major driver.

The relationship between population growth and long-term capital growth is really interesting.

The clear winner is Brisbane, multiplier of 3.4% in 40 years. Melbourne #2 at 3.8%. Perth has one of the strongest population increases, but it’s only delivered 2.6%

There is a connection, but there’s not a direct correlation. It plays a part, but it’s different for each city and location.

Other factors like government stimulus, access to finance and liveability which play a role.

How have capital city prices on the ladder changed, and which cities displayed more volatility than others?

Melbourne switches around quite a lot, at some point Melbourne is in fourth place.

What is an absolute shock was seeing Perth’s movement – by a country mile. Perth was just trailing Sydney in March 2007 – this demonstrates the power of employment, natural resources and jobs paying serous coin.

Darwin also has a similar story – mining towns that have boomed and busted.

Canberra can be quite cyclic – it does have the highest percentage of people with a university education – underpinning of reasonably solid incomes.

These are inflation adjusted – it is growth above inflation. It’s a great hedge against inflation, it will grow faster historically over the rate of inflation.

Gold Nuggets

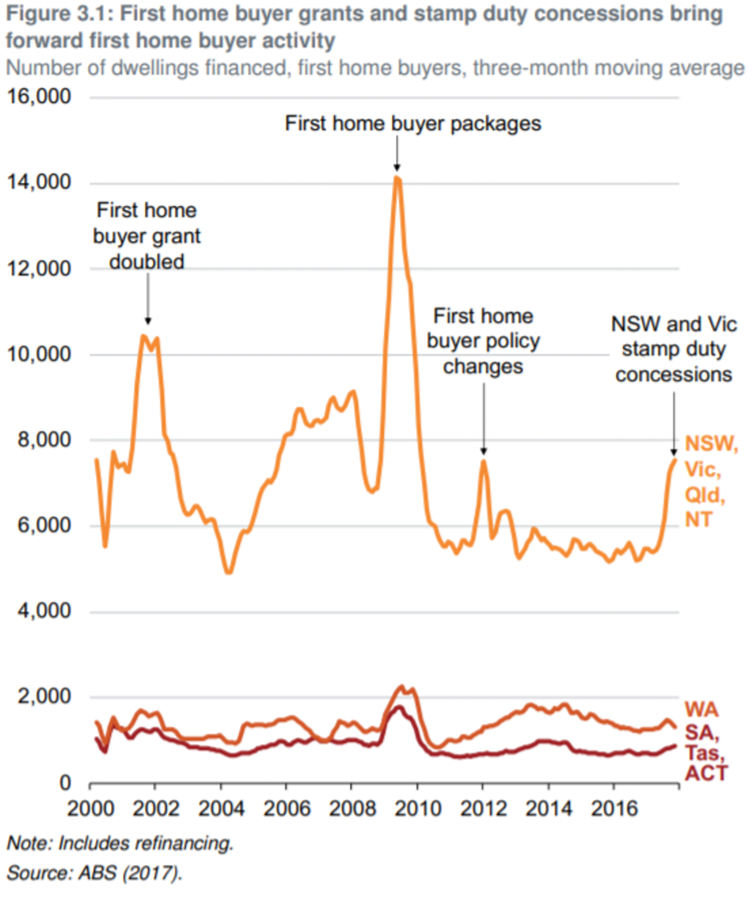

Cate Bakos – The Property Buyer’s Golden nugget: my gold nugget is about our last question that I’m going to squeeze in. What sort of influence has there been from Government incentives and initiatives? We’ve got a few charts, it certainly shows a correlation – First Home Buyer Grant, packages, policy changes, stamp duty concessions – you can absolutely see how these played out. First home owner grant and then boost after the GFC, you then see an update in the national data.

Peter Koulizos – The Property Professor’s Golden nugget: there’s a lot of scare mongering, property prices will drop by 15%-25% – if you look at the data, there has not been a time where property prices have dropped more than double digits. When you compare current interest rates, inflation and unemployment, there is no reason why they would drop by that much. If they drop by 6%, it’s no big deal. Even if you bought at the top of the boom, in a couple of years time, property will have increased anyway.

Market Updates

Quality properties garner competition despite market cycles Cate shares her experience of bidding on election weekend, which as expected, was quieter than usual as prospective buyers took to the polls and enjoyed a democracy sausage. However, one property in particular which ticked many boxes saw a very competitive auction, which reinforces the basic principle that quality properties will garner interest and competition whether the market is rising or experiencing a lull.

The results of US cash rate increases Dave shares some surprising data from the US which has gone through 14 cycles of cash rate increases and 11 recessions. Stay tuned for next week’s episode, for a comparison with Australia’s history of rate increases and how they have impacted the economy.

Government shared equity scheme Pete encourages our listeners, whether first time buyers or parents with adult kids, to check out the government’s shared equity scheme which is set to be introduced on the 1st of July this year. There will be income caps and property value limits, but for anyone looking to get a foot in the property door, this could be a good initiative.