The Real Cost of Kids – How Dependents Impact Your Borrowing Power

- Property Planning Australia

- May 12, 2025

- 4 min read

When planning to buy your family home, start your property investment journey or even consider renovations, your kids don’t just impact your bedtime routine, they also have a major influence on your borrowing power.

Whether you’re already a parent or planning for the future, understanding how dependents affect your borrowing capacity can help you make smarter financial decisions.

In today’s blog we cover:

How Your Kids Shrink Your Borrowing Power

The Hidden Cost of Having Children

The Silent Borrowing Power Killer: Taking Time Off for Parental Leave

Make Smart Property Decisions Before Expanding Your Family

The Extra Challenge for Single Parents

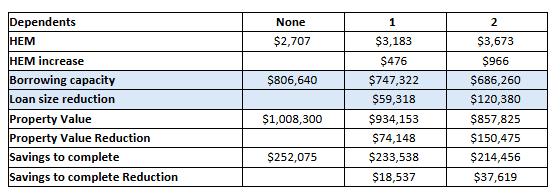

How Your Kids Shrink Your Borrowing Power

Lenders assess your ability to repay a loan based on three key factors: income, existing liabilities and living expenses.

The more you spend on daily living, the less you can afford in repayments.

One of the key tools lenders use to estimate living costs is the Household Expenditure Measure (HEM).

This benchmark helps banks gauge how much it costs to live in a household, factoring in things like food, utilities and other essentials.

Each child increases those costs, reducing your borrowing power.

The Hidden Cost of Having Children: It’s Not Just Diapers

For example, a couple earning $300,000 with no other debts could borrow approximately $1.32 million.

Add one child? That figure drops by about $35,000.

With two kids, it’s down $70,000 – and this is just based on the HEM benchmark, which adds ~$350 per child.

In reality, most families spend far more.

If each child adds $700 per month to your real-world expenses, that’s a potential $70,000 hit to your borrowing power – per child.

And if private schooling is part of the plan, expect an even bigger dent.

One child with $30,000 per year fees could reduce your capacity by over $300,000.

Two children and a total of $50,000 per year in fees and you’re looking at a $560,000 reduction.

These aren’t just numbers, they’re potential homes you can no longer afford.

The Silent Borrowing Killer: Taking Time Off for Parental Leave

Another key factor to consider when planning for children is the likelihood that one parent will need to take time away from work. This can significantly impact your borrowing power.

When transitioning from a dual-income household to a single income, your borrowing capacity can take a serious hit. For example, if one partner earns $80,000, stepping away from work could reduce your borrowing power by around $518,000.

In many cases, the partner who steps away doesn’t return to full-time work for several years or ever, which means you have just lost a great opportunity to access finance at a higher level.

It can also result in your borrowing capacity remaining restricted for an extended period, often during your peak earning years in your late 30s, 40s and 50s.

When you combine the higher living expenses that come with adding children to the mix and a drop in household income, you’re effectively facing a double whammy on your borrowing capacity.

Make Smart Property Decisions Before Expanding Your Family

In short, kids significantly affect your borrowing power and what home you can purchase.

The best time to make property decisions or at least have a Property Plan is before you expand your family, while your borrowing capacity is still high.

Whether you’re growing your family or navigating major life transitions like moving cities, becoming self-employed or switching jobs, engaging with an experienced strategic mortgage broker or property planner can help you make proactive decisions and align them with your long-term goals, before these changes impact your financial situation.

The Extra Challenge for Single Parents

The story becomes even more challenging for single parents.

With only one income to cover all the household expenses, coupled with often higher childcare and household costs, the financial burden is significantly greater.

The Household Expenditure Measure (HEM) assumes that the cost of raising children is higher for single parents, not because children are inherently more expensive, but because there’s only one adult to share the financial responsibilities.

Without a second adult to help manage the day-to-day tasks, single parents often rely more on paid services and have fewer opportunities for cost-saving. For example:

Going out with friends? You’ll likely need to hire a babysitter.

Working full-time? After-school care becomes essential.

Household chores? Tasks like gardening or cleaning, which might have been split previously, may now need to be outsourced due to time constraints.

These added expenses are reflected in the HEM figures. For a single parent, each dependent adds about $490/month to living expenses, compared to $350/month for each child in a couple household. This means that a single parent has an extra $140/month per child assumed in their living costs, directly impacting their borrowing power.

In practical terms, this means if you’re a single person earning $150,000, each child could reduce your borrowing power by around $60,000, compared to a reduction of just $35,000 for a couple in a similar financial situation.

Reach Out to Us for Expert Advice

Schedule a meeting with us to discuss your:

Mortgage Strategy

Next Purchase

Refinance

Develop a Comprehensive Property Plan

Want to Learn More About Borrowing Capacity?

Listen to #306: How to Increase Borrowing Power – How Kids, Rate Cuts and Variable Income Impact Property Buying Potential, Equity Access & Refinance